EIFS Siding and Homeowner’s Insurability in Florida: Risks, Challenges, and Practical Solutions

EIFS Siding and Homeowner’s Insurability in Florida: Risks, Challenges, and Practical Solutions

Florida homeowners face one of the nation’s toughest insurance markets, with high premiums, carrier pullouts, and strict underwriting after years of hurricane losses. For many, an often overlooked factor makes coverage even harder to obtain or afford: EIFS siding (Exterior Insulation and Finish System), commonly called synthetic stucco. While it offers energy efficiency and a sleek Mediterranean look popular in the Sunshine State, EIFS carries significant risks that lead many insurers to decline, exclude, or non-renew policies.

What Is EIFS Siding?

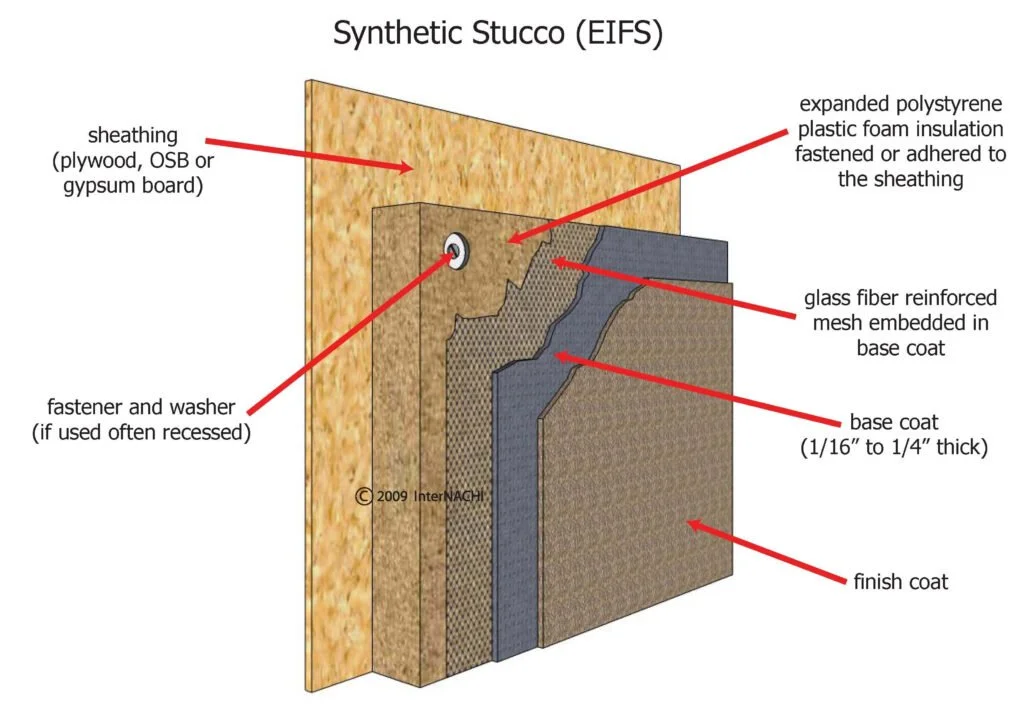

EIFS is a multi-layer synthetic cladding system consisting of rigid foam insulation board, a fiberglass mesh-reinforced base coat, and a textured acrylic finish coat. Introduced in the U.S. in the late 1960s and widely used from the 1970s onward, it provides excellent continuous insulation (often saving 20–30% on energy costs) and design flexibility for curves and details that traditional materials struggle with. In Florida, it’s frequently seen on homes built in the 1980s–2000s for its lightweight nature and stucco-like appearance.

Unlike traditional cement-based stucco (common over concrete block in Florida), older “barrier” EIFS lacks a built-in drainage plane. Water that enters through cracks, poor flashing, or penetrations (windows, doors, outlets) gets trapped against the sheathing, leading to hidden damage.

Modern “drainable” EIFS systems (post-2000 improvements) include weep holes or drainage channels, but many insurers still treat all EIFS the same due to its reputation.

Why EIFS Creates Major Insurance Problems in Florida

The core issue is moisture entrapment. In Florida’s humid, rainy, and hurricane-prone climate, this risk is amplified. Wind-driven rain, frequent storms, salt air, and intense sun accelerate cracking and deterioration. Hidden rot, mold growth, and structural weakening often go undetected until repairs become extensive and expensive sometimes requiring full recladding.

Insurers have responded aggressively. Many standard carriers outright refuse to write new policies or non-renew existing ones on homes with EIFS (especially if it covers a significant portion of the exterior or is an older barrier system). Common policy language includes broad EIFS exclusions for damage related to design, installation, maintenance, or moisture intrusion. Claims for water damage are frequently denied if tied to the siding system rather than a “sudden” peril.

As of late 2025, this remains a live issue. Specialized agencies report that even non-standard carriers may decline quickly, forcing homeowners into higher-cost surplus lines or the state-backed Citizens Property Insurance Corporation. One major Florida carrier explicitly lists EIFS as ineligible construction.

Citizens, Florida’s insurer of last resort, appears more flexible: its storm-preparation guide specifically advises homeowners to “maintain any exterior insulation-finishing system (EIFS), also referred to as synthetic stucco,” suggesting they do insure such homes when properly maintained. However, Citizens policies often come with higher base rates and deductibles, and private-market options are preferable when available.

Real-World Impacts on Florida Homeowners

Beyond coverage denials, EIFS affects insurability in multiple ways:

Higher premiums or limited options — Where coverage exists, expect surcharges or restrictive endorsements.

Resale and financing hurdles — Buyers’ lenders and insurers may balk, leading to price reductions of 20–35% in some historical cases. Real estate agents sometimes hesitate to show EIFS homes.

Claim headaches — Even covered losses can involve lengthy disputes over whether damage stems from EIFS defects versus covered perils.

Added costs — Professional inspections, maintenance, or eventual replacement add thousands to ownership expenses.

In Florida’s ongoing insurance crisis (driven by Ian, Idalia, and other storms), EIFS compounds an already challenging environment.

Steps Florida Homeowners Can Take to Improve Insurability

Don’t panic—many EIFS homes remain insurable with proactive steps:

Get a professional EIFS inspection — Hire a certified inspector for visual, moisture-meter, and infrared scanning (sometimes intrusive core samples). Update every 2–3 years or after major storms. Good documentation can sway underwriters.

Maintain rigorously — Seal cracks and joints promptly, inspect flashing and penetrations, avoid attachments that puncture the surface (mailboxes, hoses, etc.), and re-caulk every 4–5 years.

Shop specialized agents — Work with Florida independent agents experienced in high-risk properties. Some partner with carriers willing to write EIFS (often after inspection and with conditions). Avoid assuming standard carriers will decline—quotes matter.

Document upgrades — For drainable systems, provide manufacturer specs, installation certifications, and proof of proper application.

Consider replacement — The most effective long-term fix. Switching to traditional stucco, fiber-cement siding (e.g., James Hardie—highly storm-resistant and widely accepted), brick, or vinyl often unlocks better rates and broader carrier options. While costly upfront, it frequently pays for itself through lower premiums and higher resale value.

Looking Ahead: Weighing the Trade-Offs

EIFS still offers real benefits, superior insulation and curb appeal but in Florida’s insurance landscape, the risks frequently outweigh them for many owners. Modern drainable systems and strict maintenance have improved performance, yet the industry’s collective memory of past claims persists.

If you own (or are buying) an EIFS home, act early: obtain an inspection report, consult an experienced insurance agent, and explore removal if selling or refinancing soon. For new construction, strongly consider alternatives unless you’re prepared to document every detail for underwriters.

Pensacola Florida homeowners don’t have to face this alone. Partnering with knowledgeable professionals can turn an insurability headache into a manageable and sometimes avoidable issue. Protecting your home starts with understanding what’s on its walls.