Florida Home Inspections: Why Pre-2010 PEX Plumbing Could Leave You Uninsurable

Buying a home in Florida is already a high-stakes adventure—think hurricanes, flooding, and skyrocketing insurance premiums. But one hidden culprit in your plumbing system could slam the door on affordable homeowner's insurance: PEX piping installed before 2010. If you're house hunting or prepping your current property for the market, a home inspection is non-negotiable. In this article, we'll unpack what PEX is, why early versions spell trouble for insurers, and how to spot (and fix) the issues before they sink your deal. As of November 2025, with Florida's insurance market still reeling from back-to-back storms, understanding this risk is more critical than ever.

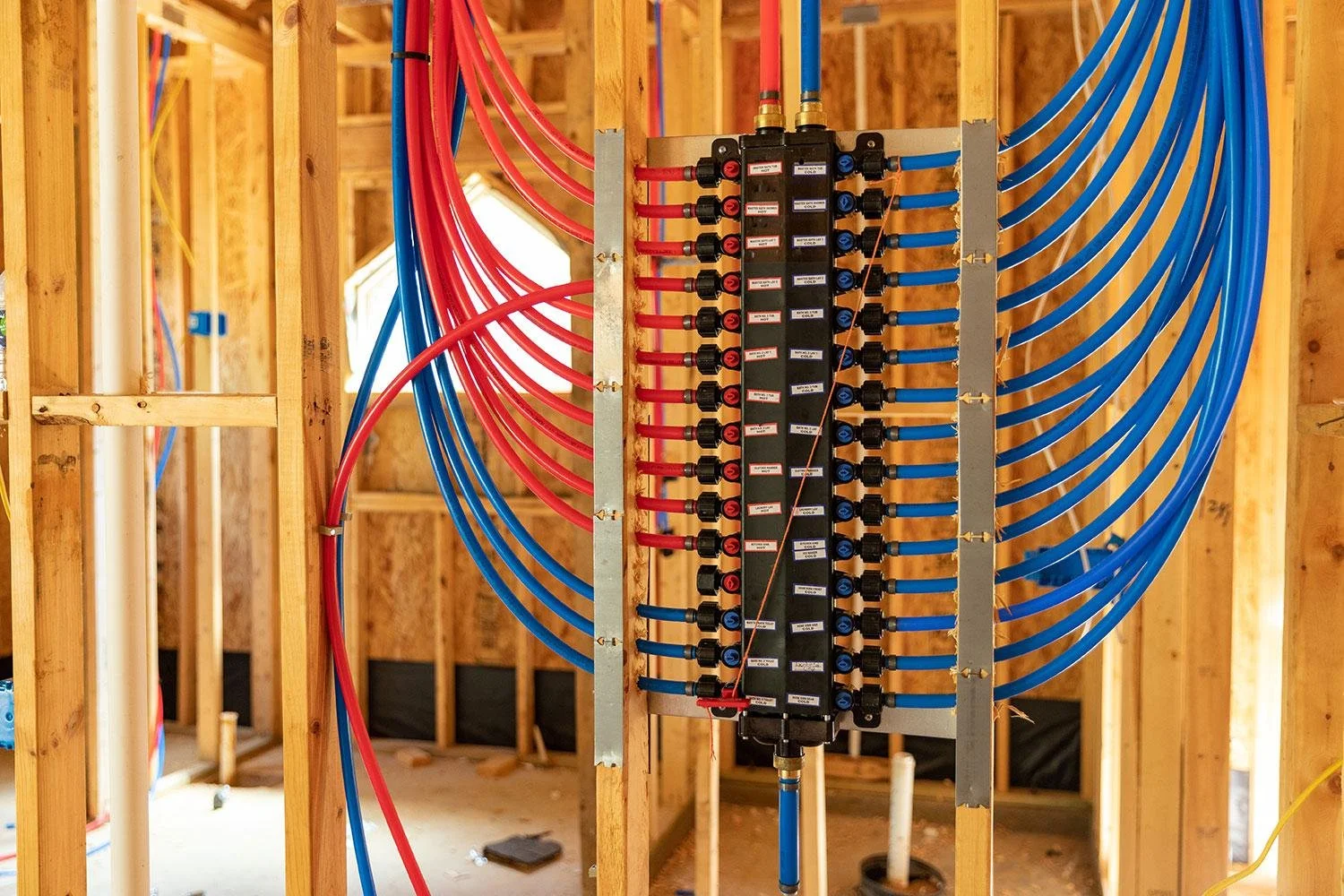

PEX 101: The Flexible Pipe That Promised the World

PEX, or cross-linked polyethylene, burst onto the scene in the 1980s as a game-changer for residential plumbing. Unlike rigid copper or PVC, PEX is flexible, corrosion-resistant, and easier to install—slashing labor costs by up to 50%. It's color-coded (red for hot, blue for cold), and its crimped or expansion fittings make for quick hookups. By the early 2000s, PEX was everywhere in Florida's booming new construction, especially in tract homes.

But not all PEX is created equal. Early generations (pre-2010) often paired the tubing with brass fittings from manufacturers like Zurn, which used ASTM F1807 standards. These fittings were cheap and compliant at the time, but they harbored a fatal flaw: dezincification. In simple terms, the zinc in the brass leaches out when exposed to Florida's aggressive water chemistry—high chlorine, minerals, and temperature swings—leaving brittle, porous metal prone to pinhole leaks.

The Zurn Debacle: A Class Action That Echoes Polybutylene Nightmares

Flash back to the late 1990s and early 2000s: Zurn's PEX systems were installed in millions of homes nationwide, including thousands in Florida. By 2007, homeowners started reporting mysterious leaks—drips turning into floods, damaging floors, walls, and ceilings. Investigations revealed the brass fittings were failing at alarming rates, often within 10–15 years. This sparked a massive class action lawsuit, *Cox v. Zurn Pex, Inc.*, filed in Minnesota federal court. The suit alleged defective design, covering homes with Zurn PEX tubing and F1807 brass fittings installed from 1995 to 2011. In 2012, Zurn settled for $67.7 million, offering affected homeowners up to $1,500 per claim for repairs—peanuts compared to the $10,000–$50,000 in water damage many faced. A separate investigation into Zurn's plastic fittings continues as of 2024, but the brass issue sealed PEX's reputation as "the new polybutylene." Polybutylene (PB) pipes? Remember those black or gray plastic lines from the 1970s–1990s that degraded under UV light and chlorine, causing a wave of failures? Insurers dropped PB homes like hot potatoes, leading to a $1 billion settlement and widespread uninsurability. Pre-2010 PEX evokes the same dread: unreliable, litigious, and leak-prone.

Why Florida Insurers Are Drawing a Hard Line on Pre-2010 PEX

Florida's insurance landscape is a perfect storm for PEX paranoia. The state already grapples with the highest homeowner's premiums in the U.S. (averaging $6,000/year in 2025), driven by hurricanes, sinkholes, and litigation-friendly laws. Insurers, burned by PB claims, see pre-2010 PEX as a ticking time bomb. Here's why they're saying "no thanks":

Failure Rates and Claims History: Studies show early Zurn fittings fail 2–5 times more often than modern alternatives, with leaks often hidden in walls until catastrophic. In humid, chlorinated Florida water, dezincification accelerates, spiking water damage claims—insurers' biggest payout category.

Underwriting Policies: Major carriers like State Farm, Allstate, and Citizens Property Insurance often exclude or surcharge PEX pre-2010. Policies explicitly state: "No PEX plumbing except in 2010 or newer homes." Others require a plumbing inspection or proof of replacement. Citizens, Florida's insurer of last resort, will cover it but at premium rates—up to 20–30% higher.

Market Squeeze: With 15 insurers fleeing Florida since 2023, competition is fierce. Underwriters err on caution; one bad PEX claim could cost $20,000+, eroding thin margins. A 2014 investigation found several firms denying coverage outright or hiking premiums by 50% for PEX homes.

Regulatory Echoes: Florida's Office of Insurance Regulation encourages risk-based underwriting, but doesn't mandate PEX coverage. Post-Hurricane Ian (2022), scrutiny intensified on "non-standard" plumbing.

Pro Tip: If you're selling, disclose PEX upfront—hiding it invites lawsuits under Florida's buyer disclosure laws.

Spotting Pre-2010 PEX During a Home Inspection: Your Red Flag Checklist

A standard home inspection ($400–$600 in Florida) should flag PEX, but not all inspectors dive deep into plumbing history. Hire an ASHI-certified pro with plumbing expertise, and request a "plumbing-only" add-on ($150–$250) including a pressure test and visual fitting check.

Inspection Essentials

Visual ID: PEX is flexible plastic tubing (1/2–1 inch diameter), often white, red, or blue. Exposed runs in basements, garages, or attics are easiest to spot. Check manifolds (home-run systems common in 2000s builds).

Fitting Forensics: Look for brass crimp rings or expansion fittings stamped "Zurn" or "F1807." Post-2010 uses improved alloys (e.g., ASTM F1960 expansion) or stainless steel.

Leak Hunt: Run water full-blast for 15 minutes; watch for drips at joints. Use a moisture meter on walls/floors near pipes. Thermal imaging ($100 add-on) reveals hidden dampness.

Age Verification: Review builder records or permits—install date is key. Pre-2010 = high risk.

Common Red Flags:

Corrosion or green patina on brass fittings.

Water stains or soft spots in drywall.

Recent "mystery" repairs around plumbing.

Homes built 2000–2009 in high-growth areas like Pensacola, FL or Navarre, FL suburbs.

If PEX is flagged, budget $5,000–$15,000 for repiping with modern PEX-A or copper—insurers often credit this toward premiums.

Alternatives and Fixes: Getting Insurable Again

Don't panic—options exist:

Repipe Proactively: Swap to PEX-B (post-2012 standards) or copper. Cost: $4–$8 per linear foot. Many insurers offer discounts for "grandfathered" upgrades.

Shop Smart: Use brokers like Insurify or Policygenius to find PEX-tolerant carriers. HO-8 policies for older homes may bend rules.

Mitigation Add-Ons: Install whole-home water shutoffs or leak detectors—some slash premiums by 10%.

Legal Recourse: If your home qualifies for the Zurn settlement (claims closed, but check for extensions), it could fund partial fixes. In 2025's market, with rates stabilizing post-Fed cuts, proactive sellers who repipe close 20% faster.

Final Verdict: Inspect Now, Insure Tomorrow Pre-2010

PEX isn't all doom—it's been in millions of leak-free homes for decades. But in Florida, where one burst pipe can cascade into mold, structural woes, and denied claims, insurers' caution is warranted. A thorough inspection isn't just due diligence; it's your ticket to affordable coverage and peace of mind.

Consult a local agent for personalized quotes, and remember: Florida's plumbing past doesn't have to flood your future. Home sweet (insurable) home awaits!